Pre-March 2006 flexible trusts

We explain the tax implications of making changes to a pre-March 2006 trust.

Legislation introduced in the Finance Act 2006 affected the inheritance tax (IHT) treatment of any Interest in Possession (IIP) trust set up on or after 22 March 2006.

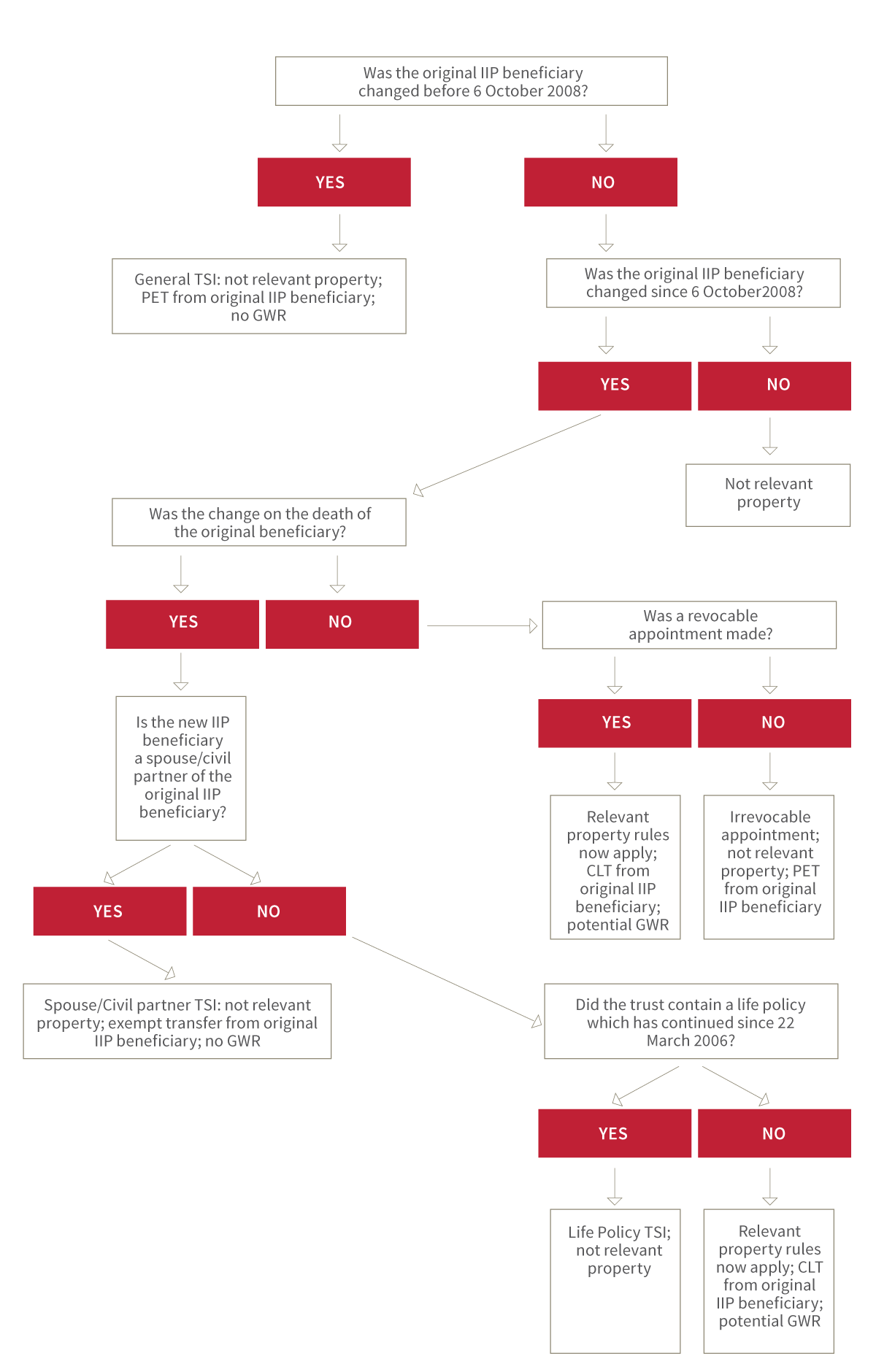

Prior to 22 March 2006, non-exempt transfers into IIP trusts were classed as potentially exempt transfers (PETs). IIP trusts allowed the trustees, and/or the settlor, the flexibility to be able to change the beneficiary. The outgoing beneficiary (sometimes referred to as having a ‘life interest’ or being the ‘life tenant’) would have been making a PET to the new beneficiary.

A transitional serial interest (TSI) was introduced whereby the original IIP beneficiary under a pre-22 March 2006 trust could be changed in certain circumstances without immediately bringing the trust into the Relevant Property Regime (RPR). Three types of TSI were made available to trustees:

- The “General TSI”

This was available until 5 October 2008 and only applied if a new beneficiary was appointed between 22 March 2006 and 5 October 2008 - The “Spouse/Civil Partner TSI”

This only applies after 5 October 2008 where the spouse/ civil partner of the original beneficiary becomes beneficially entitled to the interest following the original beneficiary’s death - The “Life Policy TSI”

This only applies to regular or single premium life policies after 5 October 2008 where the new beneficiary becomes beneficially entitled to the interest following the original beneficiary’s death

Since 22 March 2006, exercising this flexibility brought the trust into the RPR. This meant that the outgoing beneficiary would be seen as making a chargeable lifetime transfer (CLT) based on the value of the trust fund at that time, which potentially resulted in an immediate IHT charge.

As the trust has now become relevant property, and subject to the discretionary trust regime, ten-yearly anniversary charges would be triggered. However, the dates of the periodic charges would fall on the ten-yearly anniversary dates of when the original IIP trust was set up, not the tenth anniversaries from the date the trust became relevant property.

If the appointment was revocable, the transfer from the beneficiary would also be a gift with reservation (see below). Going forward, as the trust would be within the RPR, there could potentially be future 10 yearly periodic and exit charges.

Gift with reservation (GWR)

If the trustees decide to appoint benefits away from a previously named beneficiary, they will need to consider the GWR rules.

The original beneficiary could still be a potential beneficiary under the trust and so the interest would still be regarded as part of their estate for IHT purposes, even though they might never have an interest in the trust again. To avoid this, they should be removed from being a beneficiary under the “potential beneficiaries” class. Alternatively, an absolute appointment could be made, but this would remove any further flexibility.

New money

If the settlor wishes to add any further monies to the trust and the sole trust asset was a life policy, care should be taken as to whether this was an option under the policy terms at 22 March 2006.

If additional monies were not allowed under the policy provisions, any new monies would mean the whole policy would be brought in to the RPR.

Where regular premiums continue to be paid under a pre-22 March 2006 life policy held in a trust (or are varied under an option), they would continue to be treated as PETs if they fell outside any available exemptions. Similarly, where a single premium life insurance bond under a pre-22 March 2006 trust allows top-up premiums, those top-up premiums would continue to be treated as PETs. Therefore the life policy held under the pre-22 March 2006 trust would not be in the RPR.

This does not apply to capital redemption policies.

Potential solutions

The trustees could:

- Make an irrevocable appointment to the new beneficiary. This would convert the trust into a bare trust, with the original beneficiaries making a PET. Therefore there would be no IHT periodic or exit charges in the future and there would be no issues with GWR.

- Make a revocable appointment and exclude the original beneficiaries which removes the GWR problem. But remember that this would bring the trust into the RPR, meaning that the original beneficiaries are making a CLT and the trust could suffer periodic and exit charges.

- Not make any changes yet. The settlor could provide a letter of wishes. Although not legally binding, this could confirm that he wishes for the IIP to remain in force with the original beneficiary until his death, at which point the trustees could make an irrevocable appointment to a new beneficiary. This would still be a PET when the appointment takes place, but there would be no issue with GWR, nor any future periodic or exit charges.

In conclusion, if a client has a pre-22 March 2006 IIP trust, changing who has the IIP can now have major taxation consequences. Clients in this situation should therefore always be encouraged to obtain professional advice before taking any action.

The following flowchart shows the impact on changing a beneficiary’s interest on a pre-22 March 2006 IIP trust:

Changing a beneficiary’s interest:

This information is based on Canada Life’s understandings of applicable legislation, law and current HM Revenue & Customs practice as at December 2024. It is provided solely for general consideration. The information regarding taxation is based on our understanding of current legislation, which may be altered and depends upon the individual financial circumstances of the investor. We recommend that investors take their own professional tax advice.