New research from Canada Life reveals the significant improvement in annuity rates over the past 12 months has also had a positive impact on the cost of guarantees. In one example, the margin between no guarantee and a 20-year guarantee is just a 4% reduction in annual income, with a £100,000 annuity securing an income of £6,532 vs £6,270, a reduction of £262 a year. The 20-year guarantee will return income of at least £125,400, irrespective of what happens to the customer.

Nick Flynn, retirement income director at Canada Life commented:

“As annuity rates have improved so has the cost of the death benefits available. No longer do clients need to trade off a big drop in income to provide valuable guarantees. The reduction in income from choosing a longer guarantee period which effectively provides a ‘money-back’ guarantee, is now so narrow as to cost peanuts, so it’s completely bonkers not to consider some guarantees to provide additional certainty.

“Now one of the biggest barriers to annuities, ‘I won’t get my money back if I die early’, can really be challenged and guaranteed periods need to be explored. People considering annuities as part of their retirement income plan should seek the help and support of a specialist broker or regulated financial adviser. That will help ensure all options are considered in the rounds before making any irreversible decisions.”

How the costs compare - £100,000 purchase price

|

Guarantee period, (to cover early death) |

Annual Income, payable for life |

Minimum Guaranteed income |

Change in annual income to provide additional protection |

|

None |

£6,532 |

|

|

|

5 years |

£6,522 |

£32,610 |

- £10 |

|

10 years |

£6,489 |

£64,890 |

- £43 |

|

20 years |

£6,270 |

£125,400 |

- £262 |

|

30 years |

£5,879 |

£176,370 |

- £653 |

|

50% Value protection |

£6,505 |

£50,000 |

- £27 |

|

100% Value protection |

£6,388 |

£100,000 |

- £144 |

Source: Canada Life annuity rates as at 11/04/2023. Healthy life aged 65, average postcode

How the annuity guarantees choices work in practice

No guarantees. Immediately on the death of the customer, the income stops.

Spouse benefits. A customer can choose to pay anywhere between 0% and 100% of the original annuity income to a spouse, subject to a reduction in income. Upon the death of the spouse, the income stops.

Guaranteed periods. A customer can opt for any income guarantee period between 1 year and 30 years, again, subject to a reduction in the income received. In the event of the death of the customer, the income will continue to be paid to a spouse or beneficiary for the remaining guarantee period.

Value Protection (VP). A customer can choose to protect the capital purchase value of the annuity, up to 100%, again, subject to a reduction in annual income. Upon the death of the customer, the difference between income received to date and the ‘value protected’ amount is paid to the spouse or beneficiary, in the form of ongoing income or the value can be commuted as a lump sum.

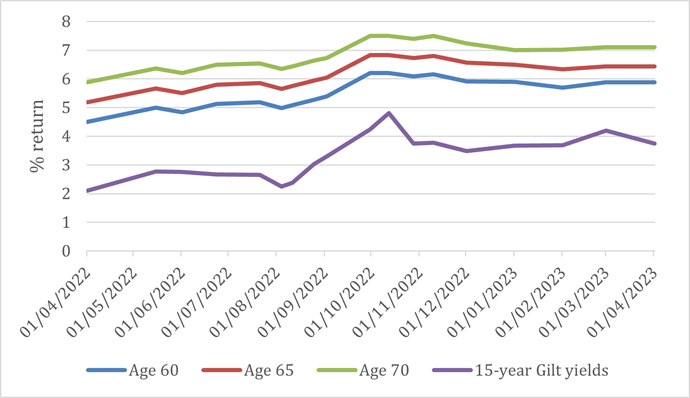

How annuity rates have changed over the last year

Source: Canada Life annuity rates over time, as at 01/04/2023

ENDS

Enquiries:

Press enquiries should be directed to:

Elle McAtamney at Canada Life, elle.mcatamney@canadalife.co.uk

Notes to editors:

- Source: Canada Life benchmark annuity rates as at 11/04/2023. Single life, £100,000 purchase price, aged 65, no health or lifestyle conditions.

About Canada Life:

Canada Life is part of a group of companies controlled by Great-West Lifeco Inc., a diversified financial services holding company headquartered in Winnipeg, Canada. Through its subsidiary companies, Lifeco has operations in Canada, the United States, and Europe. Great-West Lifeco and its insurance subsidiaries have received strong ratings from major rating agencies. Great-West Lifeco has over 30 million customers worldwide and £1.341 trillion assets under administration (as at 31 December 2021).

Canada Life Limited began operations in the United Kingdom in 1903 and looks after the retirement, investment and protection needs of individuals and companies alike. As well as providing stability and security through its individual contracts, Canada Life Limited has grown to become the leading provider of competitively priced group insurance solutions. Canada Life acquired Retirement Advantage on 3rd January 2018 for an undisclosed sum. The acquisition added over 30,000 retirement income and equity release customers and more than £2 billion of assets under management including a £1.5 billion block of in-force annuities to Canada Life.

Canada Life Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Canada Life International Limited and CLI Institutional Limited are Isle of Man registered companies authorised and regulated by the Isle of Man Financial Services Authority. Canada Life International Assurance Limited and Canada Life International Assurance (Ireland) DAC are authorised and regulated by the Central Bank of Ireland.

Stonehaven UK Limited, trading as Canada Life, is a subsidiary of The Canada Life Group (U.K.) Limited. Authorised and regulated by the Financial Conduct Authority. Registered in England and Wales. Registered number: 05487702. Registered office: Canada Life Place, Potters Bar, Hertfordshire EN6 5BA.