Need an adviser?

Get a tailored quote for this product from a financial adviser. To find one, visit Unbiased.

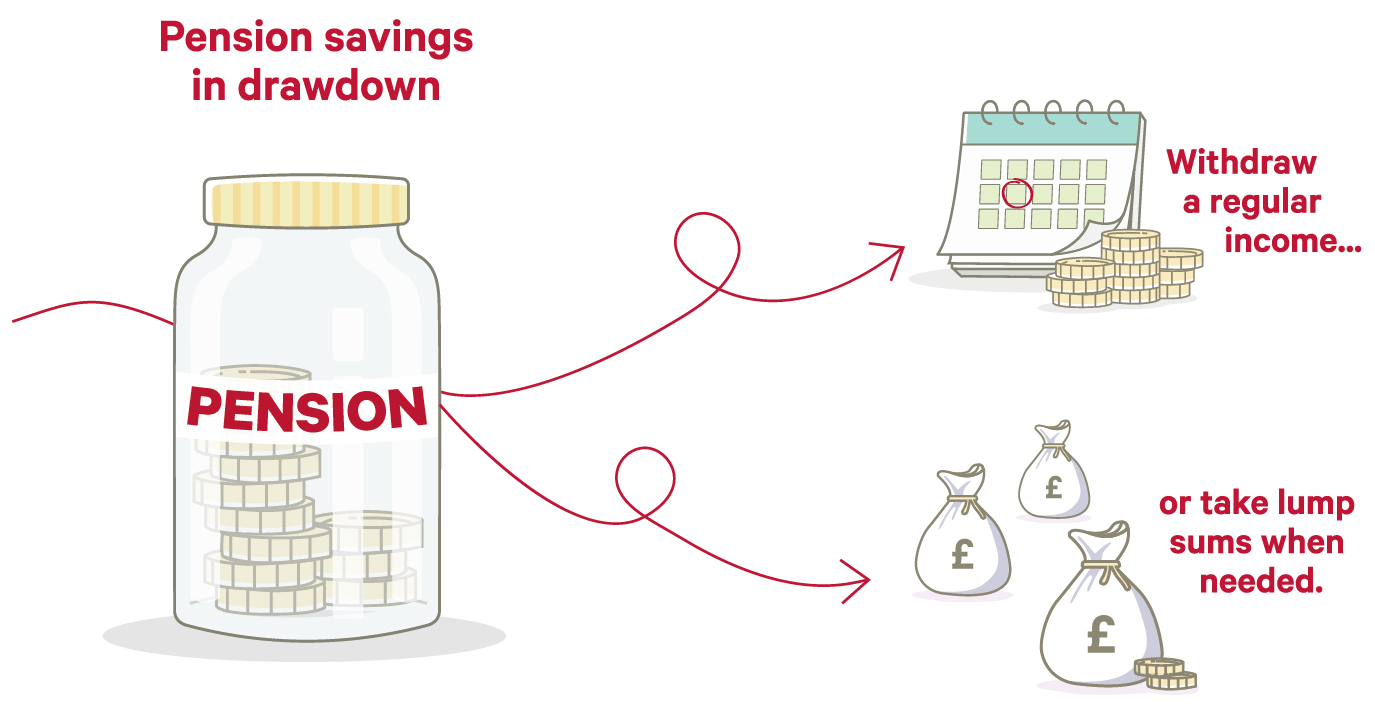

Pension drawdown, also known as flexi-access drawdown or flexible retirement income, gives you the freedom to choose when and how much to withdraw from your pension.

Please note that the information set out here is provided for guidance and education purposes only (and is not professional advice and should not be relied on). If you need help with your pension arrangements, we strongly encourage you to speak to a professional adviser. For example, an appropriately qualified FCA-regulated independent financial adviser, solicitor or tax practitioner.

Pension drawdown is a way for you to take an income from your pension when you decide to retire. Your pot stays invested, and you withdraw money from your pension savings when it best suits you.

As drawdown gives you the freedom to choose when and how much to withdraw, it’s also called flexible retirement income, flexi-access drawdown, or income drawdown.

But, because your retirement income is taken directly from your pension fund, you risk running out of money if you don’t plan carefully.

|

|

|

Potential growth |

Flexible access |

Future options |

|

Your pot is invested, giving it the opportunity to grow in value.1 This could provide protection against the effects of inflation. |

You can withdraw money from your pension as and when you need it. Take regular income or draw lump sums on an ad hoc basis. |

If your situation changes, you can convert your drawdown pension, or part of it, into guaranteed income at a later date. |

At Canada Life UK, we only provide drawdown to our existing customers. Your pension provider will be able to tell you if they offer drawdown. If they do, it’s still important to shop around to ensure you’re getting the right solution for your individual circumstances.

We always recommend speaking with a financial adviser before making key decisions about your financial future.

To put your pension savings into a drawdown, you need to :

A defined contribution scheme is a type of pension where you contribute a portion of your income to build up a pot of money. If you’re employed full time, your employer will normally also make contributions into your pension.

These are common nowadays, but you may have a ‘defined benefit pension’ if you’ve worked for the government or a large employer in the past.

Learn more about defined contribution and defined benefit pensions.

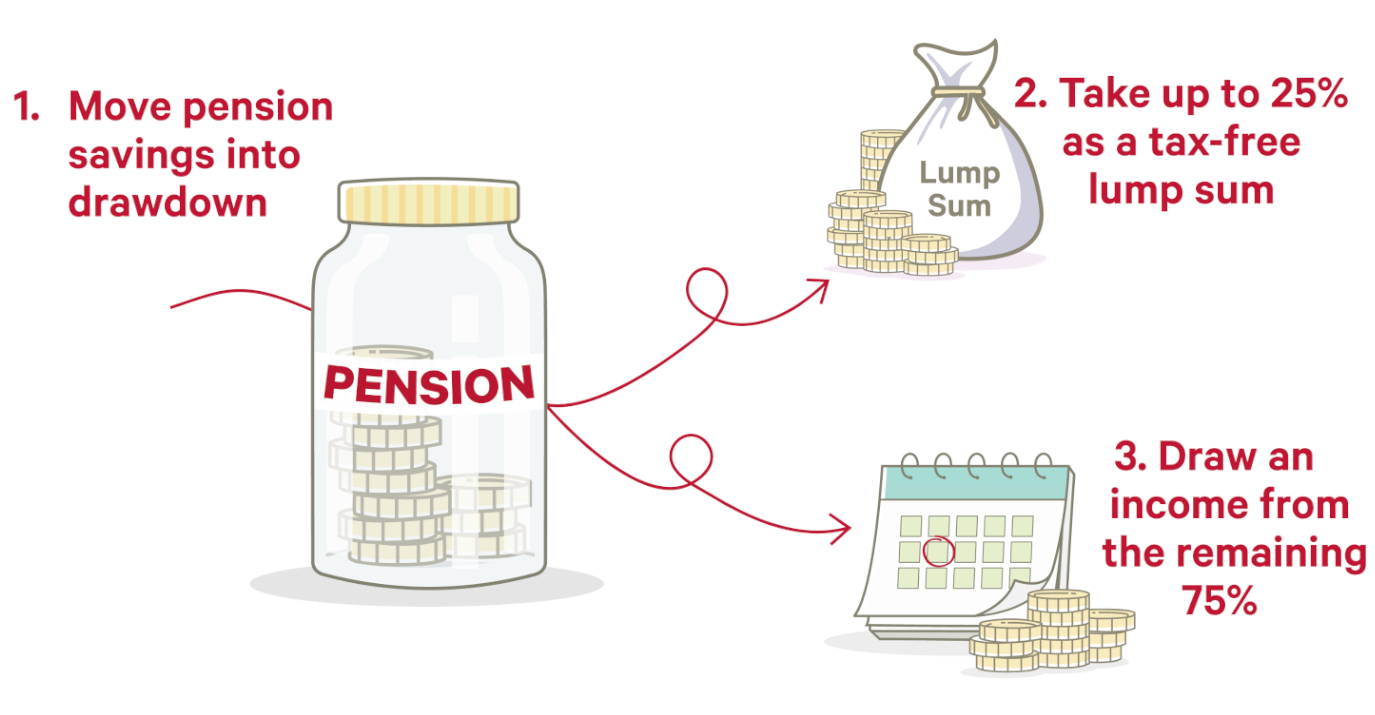

You have a range of choices when it comes to moving your pension pot into drawdown.

When you move your pension, or portions of it, into drawdown, you’re able to take a tax-free lump sum. This is called a Pension Commencement Lump Sum (PCLS), or ‘tax-free cash’.

‘Tax-free cash’ is a benefit of saving into a UK-registered pension scheme. In total, you’re allowed to access up to 25% of your pension pot tax free, normally up to a maximum of £268,275. This means you can take a lump sum from your pension when you move money into drawdown – and not pay tax on it.

For example, let’s assume your pot is £100,000 and you’d like to put the entire amount into drawdown:

If you move money into drawdown in phases, you can take up to 25% of the total amount you’re accessing each time as tax-free cash. Staying with the above example, if you decide to initially move only half of your £100,000 pot into drawdown, you can:

Your pension remains invested while it’s in drawdown. This gives it the opportunity to grow, possibly protecting its buying power against rising prices. However, investments can fall in value, too. If this happens, you’ll have less to draw an income from.

We strongly recommend getting professional pension advice from a qualified financial adviser before making any lasting decisions. An adviser will look at your entire financial situation and work with you to tailor a solution that best meets your individual needs – including how you should invest your pension when it’s in drawdown.

Learn more about how you might benefit from pension advice.

Many providers offer ‘investment pathways’ – an initiative started by the Financial Conduct Authority (FCA) in 2021. The pathways are designed to help those who move their pensions into drawdown before obtaining professional pension advice. There are four pathways, each with a different set of investments aligned with when you plan to start drawing on your pension.

Drawdown is often seen as an alternative to an annuity. When you buy a Lifetime Annuity, you’re exchanging some, or all, of your pension savings for a regular, guaranteed income that’ll last for life.

However, if you choose drawdown, your income is taken directly from your pension fund – which means you could run out of money if you don’t plan carefully.

You can convert funds in drawdown into an annuity at any time if your situation or preferences change. Unfortunately, you won’t be able to turn an annuity into a drawdown arrangement.

We suggest speaking with a financial adviser to find out which option will best suit your individual circumstances.

An UFPLS (pronounced ‘uf-plus’) is an ‘Uncrystallised Funds Pension Lump Sum’. The name may be a bit complicated, but the basic idea is quite straightforward.

What are ‘uncrystallised funds’?

Money you’ve saved into your pension pot is in an uncrystallised state until you decide to access a pension benefit. The funds that you use for the benefit then become ‘crystallised’. So, if you decide to:

the portion of your pension savings you use for these then becomes crystallised. Any portion that you haven’t used for the above remains uncrystallised.

An example will help make this clear.

Let’s say you’ve saved £100,000 into your pension, and you haven’t yet accessed any funds. In this case, the entire amount is uncrystallised.

If you then decide to take a £12,500 tax-free cash lump sum and put £37,500 into drawdown (see above), the total amount of £50,000 will have been crystallised. The other £50,000 – that you haven’t done anything with – will still be uncrystallised.

How does an UFPLS work?

Essentially, with an UFPLS, you’d take a lump sum directly from your uncrystallised savings without buying an annuity or putting funds into drawdown.

You can take your entire pot in one go, or you can keep taking lump sums until your savings are depleted.

This is the important bit: 25% of each lump sum is tax-free (up to a limit of £268,275), but the other 75% is added to your income for the year and taxed at your marginal rate. For example, if you take an UFPLS of £10,000:

Depending on your personal circumstances, taking an UFPLS can result in you paying significant tax on your pension, especially if you withdraw large sums.

By comparison, when you move pension savings into drawdown, you can access your tax-free cash without having to access taxable income at the same time.

Your drawdown pension can usually be paid to your chosen beneficiary without Income Tax. Typically, they can choose to (i) take the money as a lump sum or (ii) keep it in drawdown and take money out later.

But there are two important exceptions. Firstly, there may be a tax charge if the lump sum is above your Lump Sum and Death Benefit Allowance (LSDBA) at the time of your death. Secondly, a lump sum can also become taxable if it’s paid more than 2 years after the pension provider is told about the death.

Learn more about the LSDBA

Your beneficiary can still inherit your drawdown pension, but they’ll usually pay Income Tax when they take money out (whether as a lump sum or income). Normally, they can keep it invested in drawdown and only pay Income Tax when they withdraw.

Important changes to how pensions are treated for Inheritance Tax (IHT) will come into effect from April 2027.

Up to 5 April 2027, pensions have often been treated as outside the estate for IHT (particularly where the scheme has discretion over who receives benefits). But from 6 April 2027, most unused pension funds and death benefits will be counted as part of your estate for IHT purposes, and the person dealing with the estate (your personal representative or executor) will be responsible for reporting and paying any IHT due (if the estate is large enough to pay IHT).

Page footnotes:

Get a tailored quote for this product from a financial adviser. To find one, visit Unbiased.

Use our helpful finder tool to get support information for each of our products.

Monday to Friday, 9am to 5pm